Many UAE Free Zone businesses believe their 0% corporate tax rate is a guaranteed right. It isn’t. Under the latest 2025 regulations (including Ministerial Decision No. 229 of 2025), a misunderstood provision known as the “de minimis” rule could trigger a retroactive 9% tax on your entire income—and lock you out of tax benefits for half a decade.

At STH Financial Services, we are seeing more businesses operate dangerously close to this “cliff edge” without a safety net. Here is what you need to know to protect your status.

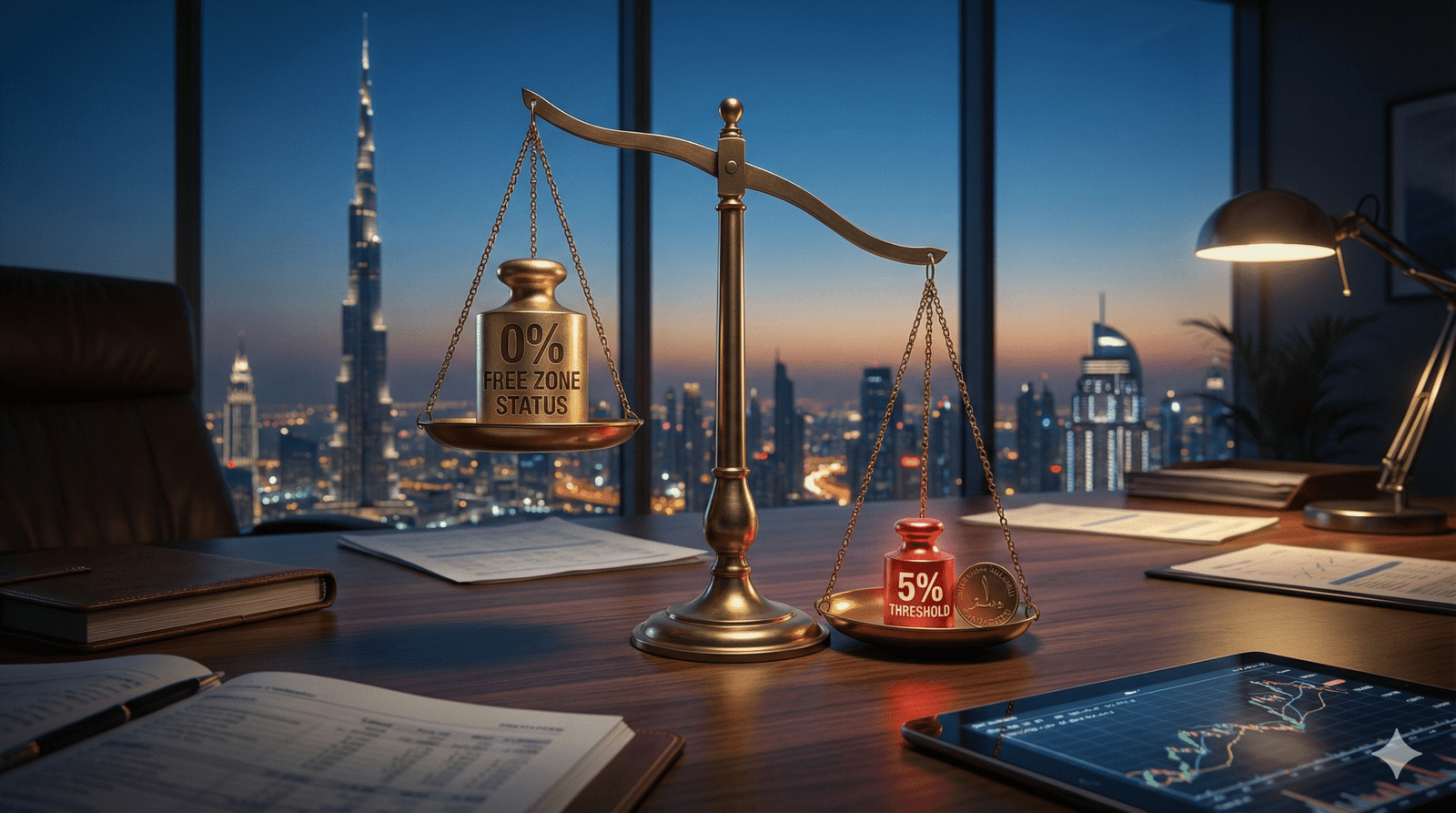

The 0% Rate is Conditional

To maintain your status as a Qualifying Free Zone Person (QFZP) and enjoy the 0% rate, you must meet strict criteria:

Maintain adequate economic substance.

Prepare audited financial statements.

Comply with Transfer Pricing rules.

Pass the De Minimis Test.

If you fail the de minimis test, you don’t just pay a small fine. You are disqualified from the 0% regime for the current tax year and the following four years.

What is the De Minimis Rule?

The Federal Tax Authority (FTA) recognizes that a Free Zone company might earn small amounts of “non-qualifying” income (e.g., small consulting fees from a mainland client or income from excluded activities).

The de minimis rule is a “buffer.” It allows you to earn this income without losing your status, provided it does not exceed a specific threshold.

The Threshold is the LOWER of:

5% of your total revenue; OR

AED 5,000,000.

The “Cliff Edge” Example

The danger lies in the “All-or-Nothing” nature of this rule.

Scenario A: The Safe Zone A Free Zone trading house earns AED 80 Million in total revenue.

5% of revenue = AED 4 Million.

Their threshold is AED 4 Million (because it’s lower than the AED 5M cap).

If they earn AED 3.5 Million from mainland services, they are SAFE. They pay 9% on the AED 3.5M and 0% on the rest.

Scenario B: The Cliff Edge The same company earns AED 4,000,001.

Because they exceeded the threshold by just 1 Dirham, they lose their QFZP status entirely.

Result: Their entire AED 80 Million is now taxed at 9%. That is a tax bill of over AED 7 Million triggered by a tiny oversight.

Common “Taints” That Breach the Threshold

What counts as “non-qualifying revenue” that can ruin your status?

Excluded Activities: Banking, insurance, and certain real estate activities.

Transactions with Natural Persons: Most B2C (Business-to-Consumer) transactions.

Mainland Income: Providing services to mainland companies that aren’t on the “Qualifying Activities” list.

Passive Income: Certain types of interest or royalties that don’t meet the “Qualifying IP” nexus.

STH Expert Insight: The 2025 “Quarterly Health Check”

From our perspective at STH Financial Services, the biggest mistake is waiting until your annual audit to check these numbers.

By the time your auditor flags a de minimis breach, it is usually too late to fix it. We recommend a “Quarterly Revenue Classification” review. By monitoring your “Qualifying vs. Non-Qualifying” mix every three months, you can pause certain mainland contracts or restructure deals before you hit the 5% limit.

When to Seek Help

The rules updated significantly in late 2025 (MD 229/2025), specifically around commodity trading and distribution. If your business model involves:

Mixed mainland and Free Zone clients.

E-commerce or B2C sales.

High-volume trading with small margins.

You need a professional QFZP Impact Assessment.

Don’t let a “small” revenue stream sink your 0% tax status. Contact STH Financial Services today for a comprehensive De Minimis Audit and ensure your business stays on the right side of the cliff.