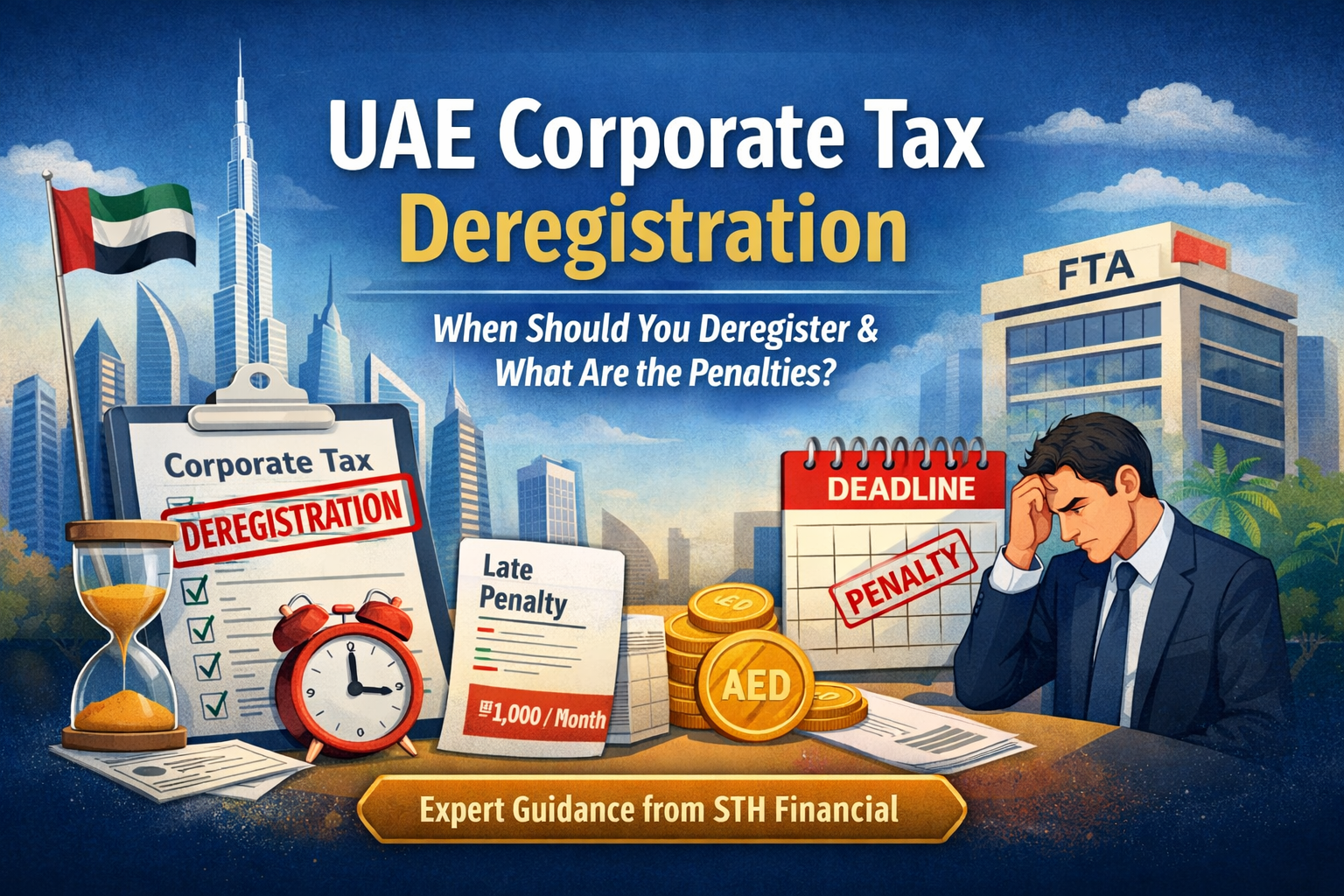

Registering for UAE Corporate Tax was a significant milestone for your business. But what happens when circumstances change and you no longer need to remain registered?

Many business owners in the UAE are unsure about the rules for deregistering from Corporate Tax—when it’s mandatory, when it’s voluntary, and what penalties apply for missing deadlines.

The question we commonly hear:

“When should I deregister from UAE Corporate Tax, and what happens if I don’t?”

Getting this wrong can result in unnecessary ongoing compliance obligations—or worse, penalties for late deregistration. In this comprehensive guide, we’ll explain everything you need to know about Corporate Tax deregistration in the UAE.

Understanding Corporate Tax Deregistration

What Is Corporate Tax Deregistration?

Corporate Tax deregistration is the formal process of canceling your registration with the Federal Tax Authority (FTA) when you no longer meet the criteria for being a taxable person in the UAE.

Why It Matters:

- Stops ongoing filing obligations

- Avoids penalties for non-filing

- Required by law when eligibility ends

- Protects your business record with the FTA

When Is Deregistration Mandatory?

1. For Natural Persons

Natural persons (individuals operating businesses) must deregister when:

| Trigger Event | Deadline |

|---|---|

| Business activities cease completely | Within 3 months |

| Revenue falls below AED 1 million threshold | Within 3 months |

The AED 1 Million Threshold:

- Natural persons with annual business income exceeding AED 1 million MUST register for Corporate Tax

- If income falls below AED 1 million, deregistration is mandatory

- Note: Once registered, natural persons cannot voluntarily deregister even if their revenue later falls below the threshold (unless they completely cease business activities)

Example:

- You registered for Corporate Tax in 2024 when your freelance income reached AED 1.2 million

- In 2025, your income dropped to AED 800,000

- You must apply for deregistration within 3 months

2. For Companies (Juridical Persons)

Companies must deregister when:

| Trigger Event | Deadline |

|---|---|

| Company is dissolved or struck off | Within 3 months |

| Company ceases to make taxable supplies | Within 3 months |

| Company becomes exempt from Corporate Tax | Within 3 months |

Important Note for Companies:

Unlike natural persons, companies do NOT have a revenue threshold for mandatory deregistration. A company remains subject to Corporate Tax regardless of revenue unless it:

- Completely ceases operations

- Is dissolved

- Qualifies for an exempt status (e.g., becomes a Qualifying Public Benefit Entity)

3. When Exempt Status Is Acquired

If your business becomes eligible for a Corporate Tax exemption (such as becoming a Qualifying Investment Fund or Qualifying Public Benefit Entity), you must apply for deregistration within the required timeframe.

When Is Deregistration Voluntary?

For Natural Persons

Natural persons CANNOT voluntarily deregister—they can only deregister when:

- Completely ceasing business activities, OR

- Falling below the AED 1 million threshold

Important: Even if your income drops significantly, once you’re registered, you remain registered until one of these triggers occurs.

For Companies

Companies generally cannot voluntarily deregister unless they:

- Cease to exist as a legal entity

- Stop making taxable supplies entirely

- Qualify for exempt status

There is no “voluntary” deregistration option simply because revenue decreased.

The Deregistration Process: Step by Step

Step 1: Determine Your Eligibility

Questions to Ask:

- What type of entity are you? (Natural person or company)

- What triggered the need to deregister?

- Have all tax returns been filed up to the deregistration date?

Step 2: Gather Required Documents

For Natural Persons:

| Document | Purpose |

|---|---|

| Copy of passport/Emirates ID | Identity verification |

| Trade license (if applicable) | Business confirmation |

| Tax Registration Number (TRN) | Account identification |

| Final tax return (if filed) | Compliance confirmation |

| Closure documents (if applicable) | Proof of cessation |

For Companies:

| Document | Purpose |

|---|---|

| Company trade license | Business confirmation |

| Tax Registration Number (TRN) | Account identification |

| All filed tax returns | Compliance confirmation |

| dissolution documents (if applicable) | Proof of closure |

| Board resolution (for deregistration) | Authorization |

Step 3: Submit the Application

Where to Apply:

- Through the EmaraTax portal

- Select “Corporate Tax” > “Deregistration”

- Complete the required form

- Upload supporting documents

FTA Processing Time:

- Standard processing: 30 business days

- May be extended if additional information is required

Step 4: Confirmation from FTA

Once approved:

- Receive deregistration confirmation from FTA

- Note the effective date of deregistration

- Retain confirmation for your records

Deadline: Critical Timeframes

Natural Persons

| Scenario | Deadline |

|---|---|

| Cease business completely | 3 months from date of cessation |

| Fall below AED 1M threshold | 3 months from end of financial year where threshold was breached |

Important: The 3-month deadline is strictly enforced. Missing this results in penalties.

Companies

| Scenario | Deadline |

|---|---|

| Dissolution/strike off | 3 months from date of dissolution |

| Cease taxable supplies | 3 months from date activities stopped |

Penalties for Late Deregistration

Penalty Structure

| Violation | Penalty |

|---|---|

| Late deregistration application | AED 1,000 per month |

| Maximum penalty | AED 10,000 |

| Continuing violation | Penalties accrue until application is submitted |

Example:

- Business ceased in January 2026

- Deregistration application submitted in August 2026 (7 months late)

- Penalty: 7 × AED 1,000 = AED 7,000

Comparison: Registration vs. Deregistration Penalties

| Issue | Registration Penalty | Deregistration Penalty |

|---|---|---|

| Late registration | AED 10,000 | N/A |

| Late deregistration | N/A | AED 1,000/month (max AED 10,000) |

Key Difference: The FTA penalty waiver program applies to LATE REGISTRATION but NOT to late deregistration. There is currently no amnesty for late deregistration applications.

What Happens After Deregistration?

Obligations That End

Once deregistered:

- No longer required to file Corporate Tax returns

- No more Corporate Tax payment obligations

- FTA compliance inquiries should cease

Obligations That May Continue

Even after deregistration, you must:

- Keep records for 7 years (from the last filed return)

- Be prepared for any outstanding tax inquiries

- Re-register if circumstances change

Re-registration

If your situation changes and you again meet registration criteria:

- You can re-apply for Corporate Tax registration

- There is no “cooling off” period

- Must meet all standard registration requirements

Example:

- Natural person deregistered when income fell below AED 1M

- Two years later, income again exceeds AED 1M

- Must register again (no penalty for re-registration)

Common Mistakes to Avoid

Mistake 1: Assuming Deregistration Is Optional

Reality: If you meet the criteria, deregistration is mandatory. Continuing to remain registered when you’re no longer required creates unnecessary compliance burden—and can cause confusion during FTA audits.

Solution: Review your status annually and apply for deregistration when eligible.

Mistake 2: Missing the 3-Month Deadline

Reality: Many businesses assume they can apply anytime. The 3-month deadline is strictly enforced, and penalties accumulate monthly.

Solution: Calendar your deadline as soon as you know deregistration is required.

Mistake 3: Not Filing Final Returns

Reality: Deregistration doesn’t excuse you from filing returns for periods where you were registered. All tax periods up to the deregistration date must be properly filed.

Solution: File all outstanding returns before submitting deregistration application.

Mistake 4: Natural Persons Assuming Voluntary Deregistration Is Possible

Reality: Natural persons cannot simply choose to deregister because they want to. The law specifies exactly when deregistration is permitted.

Solution: Understand your specific legal position—if in doubt, consult a tax advisor.

Mistake 5: Destroying Records After Deregistration

Reality: You’re still required to maintain records for 7 years after your last tax period, even after deregistration.

Solution: Maintain proper documentation even post-deregistration.

Case Studies

Case Study 1: Natural Person Falling Below Threshold

Situation: Ahmed is a freelance consultant registered for Corporate Tax since 2024. In 2025, his business income dropped to AED 800,000 (below the AED 1M threshold).

Action Required: Ahmed must apply for deregistration within 3 months of his financial year-end where income was below threshold.

If He Misses Deadline:

- Applies 6 months late

- Penalty: 6 × AED 1,000 = AED 6,000

Case Study 2: Company Dissolution

Situation: ABC Trading LLC (a mainland company) decides to close its business and liquidate in June 2026.

Action Required: ABC Trading must apply for deregistration within 3 months of dissolution.

Process:

Case Study 3: Natural Person Ceasing Business

Situation: Sarah operates a small business and decides to close it entirely in March 2026.

Action Required: Sarah must deregister within 3 months of cessation—regardless of what her income was.

Note: Even if she had no income in the final year, she must still apply for deregistration.

Checklist: Before You Apply for Deregistration

- Ensure all Corporate Tax returns are filed up to the deregistration date

- Calculate and pay any outstanding tax liabilities

- Gather required identification documents

- Prepare supporting documents (closure documents if applicable)

- Calendar the 3-month deadline

- Confirm your deregistration reason is valid under the law

- Plan to maintain records for 7 years after deregistration

Frequently Asked Questions

Q: Can I deregister from Corporate Tax if my revenue is still high?

A: For companies: No—you cannot voluntarily deregister just because revenue decreased. Deregistration only applies if you cease operations or qualify for exempt status.

For natural persons: No—if your income exceeds AED 1 million, you must remain registered.

Q: What if I don’t know when my revenue fell below the threshold?

A: For natural persons, the deadline starts from the end of the financial year in which your revenue fell below the threshold. Keep track of your income throughout the year.

Q: Can the FTA reject my deregistration application?

A: Yes, if:

- Outstanding tax returns or payments exist

- Documents are incomplete

- Additional information is required

- The trigger event is not established

Q: Is there a fee for Corporate Tax deregistration?

A: No—there is no government fee for deregistering from Corporate Tax. The only costs are potential penalties if you miss the deadline.

Q: After deregistration, am I still considered a “taxable person”?

A: No—once deregistered, you are no longer a taxable person for Corporate Tax purposes. However, if your circumstances change, you may need to re-register.

Q: Can I transfer my Corporate Tax registration to another emirate?

A: No—Corporate Tax registration is federal, not emirate-specific. There is no “transfer” process. You would deregister in one emirate and register again in another if needed.

Q: What happens if I re-register after deregistration?

A: There is no penalty for re-registering. However, you must meet all standard registration requirements. Your compliance history from before deregistration may be considered.

Conclusion

Corporate Tax deregistration is a straightforward process when you understand the rules—but it requires attention to deadlines and proper documentation.

Key Takeaways:

Don’t ignore your deregistration obligations. If you’re eligible, apply promptly to avoid accumulating penalties.

Need Help With Corporate Tax Deregistration?

At STH Financial, our tax specialists help UAE businesses:

✓ Determine if deregistration is required or possible

✓ Complete the deregistration application correctly

✓ Meet deadlines and avoid penalties

✓ File final tax returns

✓ Maintain proper records post-deregistration

📞 Contact us for assistance with your Corporate Tax deregistration.

Get Expert Help | Visit STH Financial

Related Articles: